Finance

-

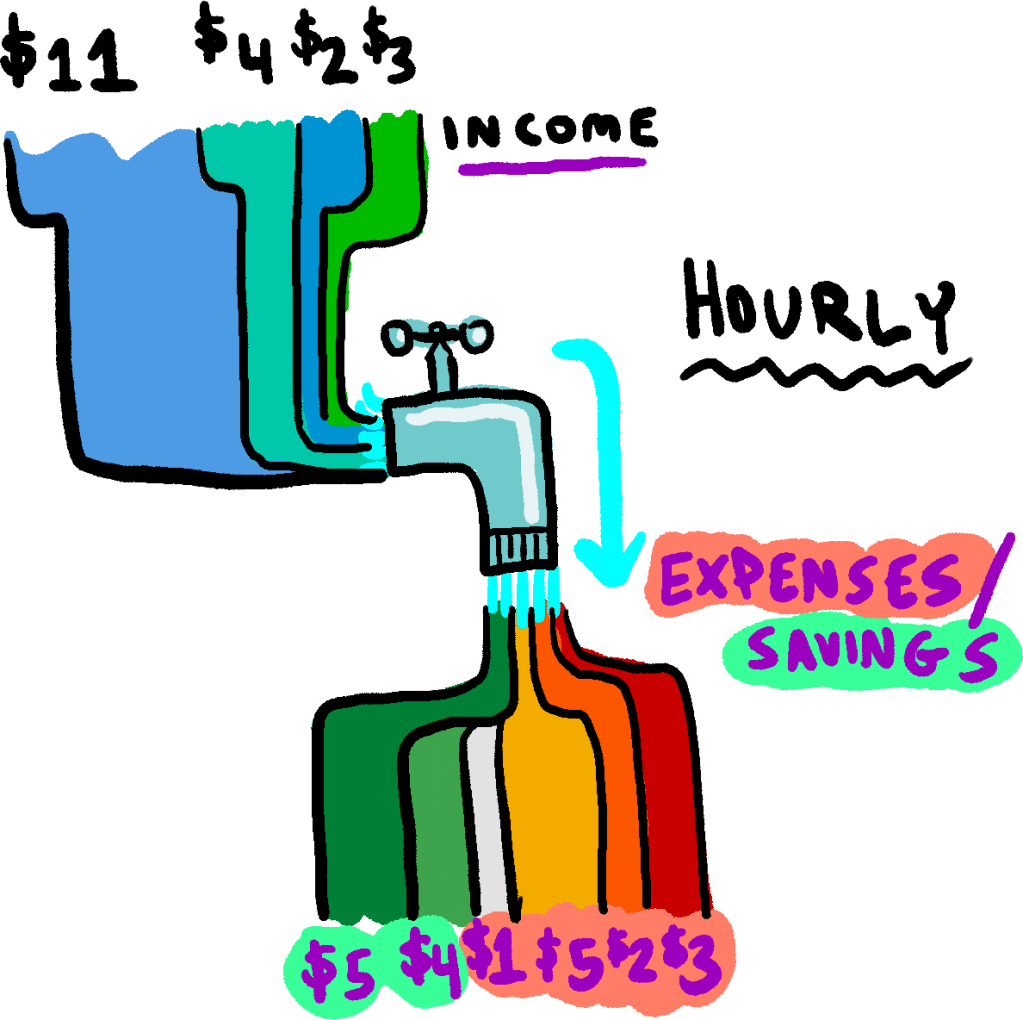

The Issue: Income sources and expenses often operate on mismatched schedules. For example, a person might receive a paycheck every two weeks, but need to pay rent monthly and car insurance every six months. These differing schedules can make it difficult for a person to visualize their cashflow. There are lots of ways to visualize…

-

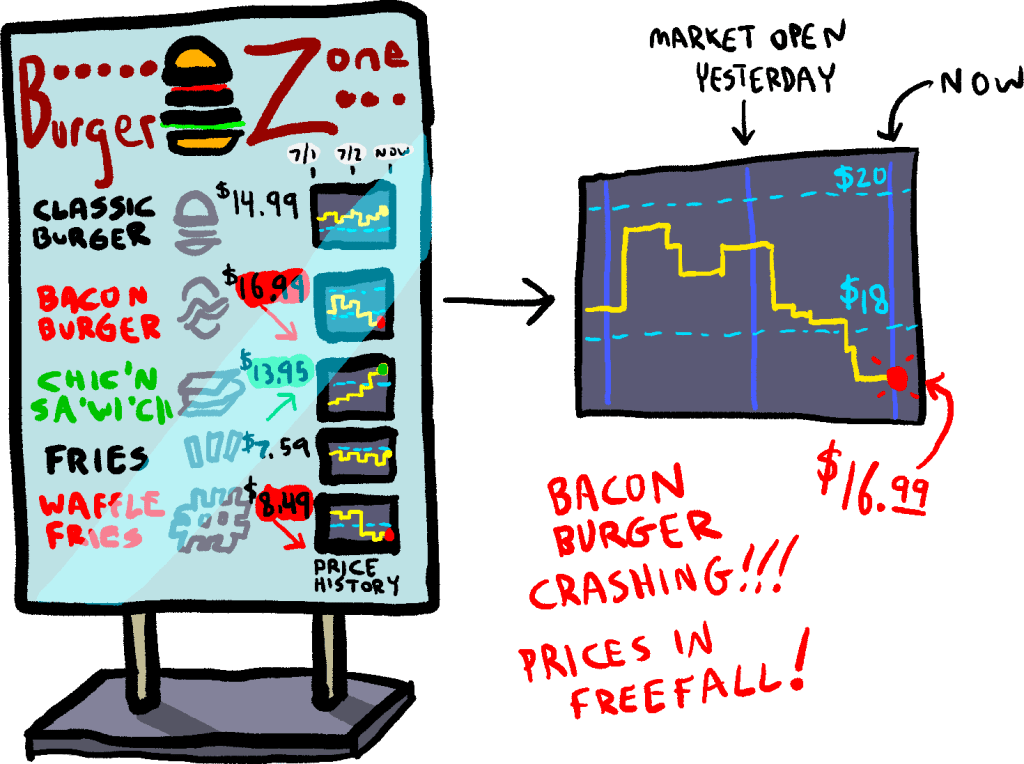

Background: Sometimes, restaurant menus will list a dish as “market price,” rather than giving a specific set price. (This is most commonly seen for seafood.) In such a situation, a diner would have to inquire as to what the specific price would be on a given day, based on the relative supply and demand of…

-

Background: Imagine the following situation: Person A has a high-paying job, but their cousin, Cousin B, has a badly-paying university lecturer job. Cousin B’s home’s roof starts leaking, and as a result of having to pay for repairs, Cousin B will no longer be able to afford to visit family for the holidays. The roof…

-

Background: “Tipping” is an additional fee paid for certain types of purchases in some countries. It is especially common in the food service industry in the United States. In theory, tips are supposed to either go to the worker who provided a certain service, or to go to a “tip pool” where tips are averaged…

-

Background: A large class of investments work as follows: you, the investor, lend a chunk of money to a borrower, who then pays it back (hopefully) over time with a bit of extra interest. Example: a city issues a $1200 bond that pays $350/year for four years (total: $1400, unless the city goes bankrupt: https://www.google.com/search?q=cities+that+went+bankrupt.)…

-

Background: The concept of buying a “stock” is that the buyer becomes a partial owner of a company and its assets. The Issue: However, there is no option to buy a stock-like investment in a particular sub-product of a company. This is surprising, since so many bizarre and creative “financial instruments” exist: you’d think someone…

-

Background: Some products, like printers, razors, and coffee machines, rely on a recurring purchase of input materials (ink, razor blades, and coffee, respectively). Frequently, the company that sells the durable part of this system will sell it at cost (or even below!), with the hope of profiting from a hefty markup on the consumables (Figure…

-

Background: Most countries have laws that discourage public officials from being financially compensated to use their official powers to benefit particular companies. (This is usually called “bribery.”) For example, a state governor probably couldn’t declare July 5 to be “Official BestUsedAutoDeals.com Appreciation Day, Use Referral Code AUTO4U.” However—maybe there’s a “one weird trick”-style loophole that…

-

Background: In the mid-2010s, video game companies discovered that they could often make more money by giving away games for free (!) and selling cosmetic “extras” than they would have made by just selling the games. These cosmetic extras are generally fairly basic (e.g. “your character is now dressed as a vampire” or “your sword…

-

Background: A huge number of books, blogs, and web sites have been written to supply investment advice to the common people. Almost all of these books recommend strategies that, up to that point, have been successful. Strangely, very few of them recommend strategies that have lead to catastrophic financial failure, even if the strategies behind…