Background:

When a company offers a rebate (“buy this widget, get $50 back”), only a fraction of customers will actually deposit the rebate check.

If customers don’t deposit their rebates, then the company can keep the money.

So it would be useful if there was some sort of dirty trick to reduce rebate deposit rates. Read on for details!

(Note: this is not a novel idea—it was inspired by an intentionally bizarre rebate check I received that could not be deposited online by at least two different banks.)

Proposal:

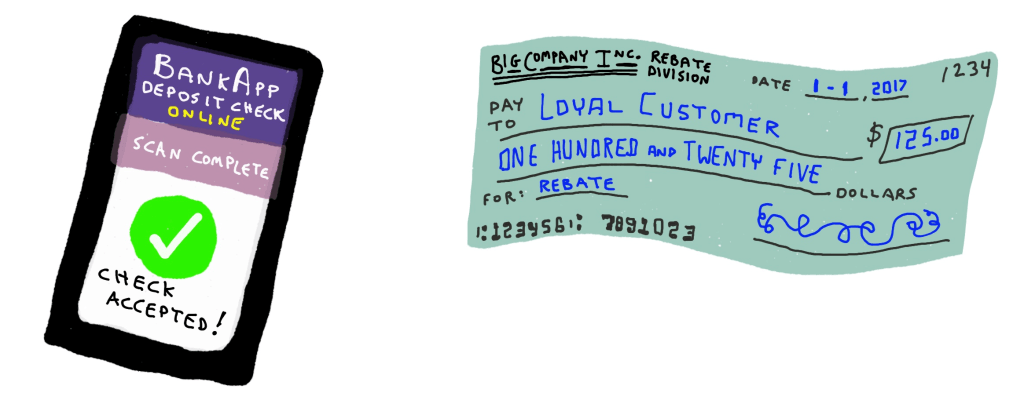

Normally, when a customer receives a rebate, it’s standard-format check (Figure 1). The customer’s banking app certainly knows how to read this format, so it is deposited with no problems.

Fig. 1: The BankApp online deposit system has no problem reading this straightforward check.

The rebate-issuing company may really want the check to fail the depositing process (Figure 2), which adds hassle and inconvenience for the check-depositing customer.

Fig. 2: If the customer’s banking app can’t read the check, then the check is much less likely to be deposited: now the company will never have to pay out the rebate! (Unless the customer actually goes to an ATM or bank branch.)

So the solution is simple—tweak the format of the checks a bit (whatever is still allowable within the law and/or banking agreements) and try to make a new check that is:

- Legal!

- This is the most important aspect—the company’s checks definitely need to be 100% legal, so the company can later blame the customer instead of taking responsibility.

- Acceptable to the banks and/or conforms to whatever check-format specifications exist

- Difficult for a computer to read (so it can’t be deposited online)

- Superficially OK looking to a human, so it isn’t obvious that the check wasn’t intentionally made to be difficult to deposit

- Also, this gives plausibly deniability to the whole business: if the company is called out on its actions, a PR person can go online and post “Oh, we didn’t realize that our rebates couldn’t be deposited online. What an unintentional—yet profitable—oversight!”

Popular ways of doing this may include:

- Weird check sizes

- Strange watermarks leading to odd contrast

- Superfluous extra characters in the deposit-amount field (like “AMT: ****123.45 $” instead of just “$123.45”)

- Irregular size (some checks are more square-shaped than “check” shaped)

- Odd or elaborate font choices

Conclusion:

Although the specific checks depicted below (Figs. 3 & 4) probably violate the “check” specifications somehow, they may be useful for inspiration.

Fig. 3: This check looks vaguely legitimate to a human, but an online deposit app is unlikely to be able to read it.

Fig. 4: Can a check be a weird futuristic hexagon? Probably not! Customers will definitely know they’re being scammed if they receive weird checks like this one.

PROS: Saves money on rebate checks! Rebates can be made more generous, since it’s now extra-difficult for anyone to redeem them.

CONS: Customers might find out about it and get slightly annoyed and call the company’s customer service line to complain. If each rebate-receiving individual wastes 20 minutes of customer service time complaining, this check technique might no longer be profitable.

You must be logged in to post a comment.